The era of tokenization — market outlook on a $24trn business opportunity

10 years after the release of Satoshi Nakamoto’s whitepaper called “Bitcoin: A Peer-to-Peer Electronic Cash System” triggered the agreed-on period for the invention of blockchain technology, blockchain is still a very young technology with low levels of mainstream adoption. Despite its commonly agreed-on disruptive characteristics, to date, we have only seen the first steps of this potential focusing on the development of basic blockchain protocols such as Bitcoin, Ethereum, or EOS. If we draw the analogy to the internet we can refer to the current state of the development of the HTML standard in 1993, facilitating the World Wide Web as we know it nowadays. As the internet needed three development stages to unfold the Web 2.0 including companies like Facebook and Twitter, we expect the Blockchain technology to take a similar journey to a tokenized asset market of ~$24trn by 2027. We came to this number by conducting a global market simulation.

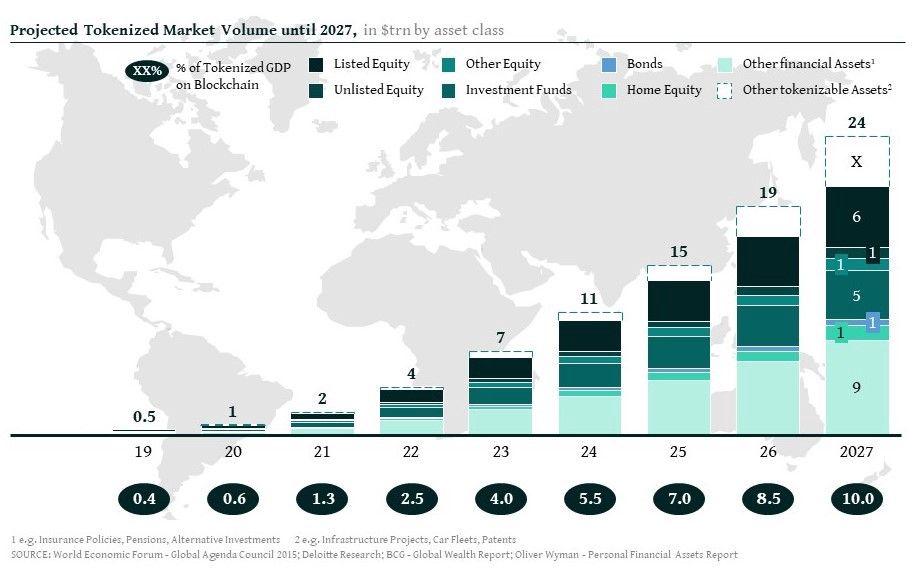

Projection of tokenized assets 2019–2027

Research and surveys from institutions such as the World Economic Forum (WEF), Deloitte, or McKinsey (see table of sources for more detail) project that up to 10% of the global Gross Domestic Product (GDP) will be stored and transacted with the help of blockchain technology by 2025–27. With this tipping point in mind, we ran a market simulation to determine the potential market size of a global tokenized market using a conservative approach.

For estimation purposes, we only looked at financial assets as well as real assets clustered into: listed equity, unlisted equity, other equity, bonds, home equity as well as other financial assets.

Based on certain factors such as past performance as well as future growth expectations per asset class, we projected the market size of the individual assets from a bottom-up perspective. In a second step, we applied different assumptions of the individual rate of tokenization per asset class and finally matched our bottom-up results with the top-down research from the WEF.

Following this methodology, we project a tokenized asset market of ~$24trn of financial assets only in 2027. This does not include currently not measured (or not existing) asset classes or unidentified tokenization use cases of intangible assets (e.g. patents, usage rights), where we expect significant innovation and growth.

Getting to significant market size, however, will take a longer journey. With currently $0.3trn and 0.3% of the GDP stored or transacted on the blockchain and almost solely consisting of the early crypto-currencies, we expect a slower increase over the next 2 years, reaching $1.0trn or 0.6% of global GDP in 2020 and $2.0trn (1.3% of global GDP) in 2021. In 2021, anticipating an acceleration of mainstream adoption of blockchain technologies, we expect accelerated growth which will lead to an additional ~1.5% of GDP per year to be stored and transacted on the blockchain. Overall, this will trigger a market growth from ~$4.0trn in 2022 to ~$24.0trn in only 5 years (2027) — an average of an additional ~$4.0bn per year at a CAGR of ~40%.

Market growth hereby will be driven by different asset classes and growth in a variety of assets stored and transacted on the blockchain with cryptocurrencies losing their primacy. Exemplary of this development, we are already seeing the slow emergence of security tokens (STOs) replacing typical utility tokens and ICOs.

From our point of view, we will see a development in consecutive waves:

Short-term: Tokenization will especially affect standardized issuing products such as Equity or Bonds — benefitting from significantly lower issuance and transaction costs (e.g. substitution of traditional IPOs with STOs). Subsequently, we expect accelerating tokenization of smaller as well as more illiquid and non-fungible assets (e.g. SME shares or Real Estate) — attributed to the benefit of easy ownership transfer leveraging the blockchain technology.

First examples of this are already present in the market:

- ICOs/STOs: Telegram raising $1.7bn in a pre-sale substituting an IPO (February 2018)

- Debt: Landesbank Baden-Württemberg (LBBW) and Daimler testing blockchain for launch of a 1 year corporate “Schuldschein” (Eng. certificate of debt), with volume of €100mn (June 2017)

- SME shares: Mt Pelerin issuing its equity digitally on the blockchain in the form of tokens and in accordance with Swiss law (October 2018)

- Real Estate: Amiran Group tokenizing Manhatten property of more than $30mn value on Ethereum blockchain (October 2018)

- Trade Finance: HSBC and ING performing trade finance transactions for Cargill using blockchain platform (May 2018)

Medium- or long-term: We will see tokenization of an additional range of ownership or usage rights, amongst others, which are stored and transacted on the blockchain. Use cases hereby can range from Infrastructure Projects/Project Finance to Legal Documents or Patents — with several use cases nowadays not even thought of. The Era of Tokenization has the potential to do to ownership rights, what digitalization did to media.

Following several academic growths scenarios, all three waves will come with increasing volumes in tokenization. Aligned with our expectation, tokenization is going to especially benefit equity offerings, the setup of tokenized investment funds as well as a very significant share from other financial assets, including all kinds of alternative assets with Private Equity, Hedge Funds and Venture Capital leading the way.

Clearly, 2027 will as well only mark a sublevel in an overall bigger picture. Whereas forecasting beyond the next years seems very hard, we are certain that The Era of Tokenization will further accelerate (especially in real assets such as home equity or infrastructure projects) and will enable completely new working/business models in our day-to-day lives (e.g. tokenization of shared fleets within cities).

Either or, we have exciting years and decades ahead of us where “The Era of Tokenization” will change the financial system as we currently know it.

Methodology

Participating in the digital asset space for a significant period relatively and being curious about different academic views on market forecasts for financial assets, we have not yet been able to find substantial and factual research. This led us to investigate, conduct and publish our own.

Our approach combines a top-down scenario based on the estimation of 10% being stored and transacted on the blockchain by 2027 (WEF) and a bottom-up growth scenario of individual assets. Hereby, we not only take established crypto-currencies into account but a holistic view of all financial and real assets to be potentially tokenized in the forthcoming future.

Referencing other relative research on global wealth, we forecasted private financial assets (PFA) on a single asset segmentation incl. Home Equity up to 2027. For the asset split, we went with the split of the Boston Consulting Group Wealth Report from 2017. Based on this, we translated the estimation of 10% stored on the blockchain from GDP to PFA — providing us with a top-down assumption of the total financial tokenized market. In this top-down estimation, we matched against a bottom-up perspective when individually forecasting the rate of tokenization for the individual asset classes and achieving a consensus of both scenarios of a tokenized market size of ~$24trn by 2027.

In contrast to other papers, this approach reflects a way more granular and simultaneously holistic thinking. Comparable papers follow a somewhat standardized approach using the quantity theory of money to deduce the value of crypto assets in need to support a forecasted economy and DCF models to estimate the value of networks that provide a yield (e.g. The Satis Group). Other research simply uses the adoption of the internet as a proxy and portrays this as the blockchain technologies (e.g. Tim Draper at DealStreetAsia PE-VC Summit, Singapore). Nearly all of them are hereby solely focusing on crypto assets which is, among other factors, another key differentiator of superior research.